Joining forces for innovation to take up challenges in the TWh era

Robin Zeng, founder and chairman of CATL, delivered a speech at the GGLB & Electric Vehicle Annual Conference

Good evening ladies and gentlemen. Today, I am pleased that I have the opportunity to give a speech here.

My speech will mainly focus on three parts: seizing the opportunities for global green recovery, innovation leading to core competitiveness, and industrial chain coordination to take up new challenges.

Seizing opportunities for global green recovery

Embracing the new energy revolution has become a global consensus, and that brings us to think of how to seize opportunities for global green recovery. In Europe, lithium-ion battery sales have performed very well this year, and sales will be increasingly better in the coming years. However, customers require that the lithium-ion battery cost must be very low, with a target to replacing fuel vehicles.

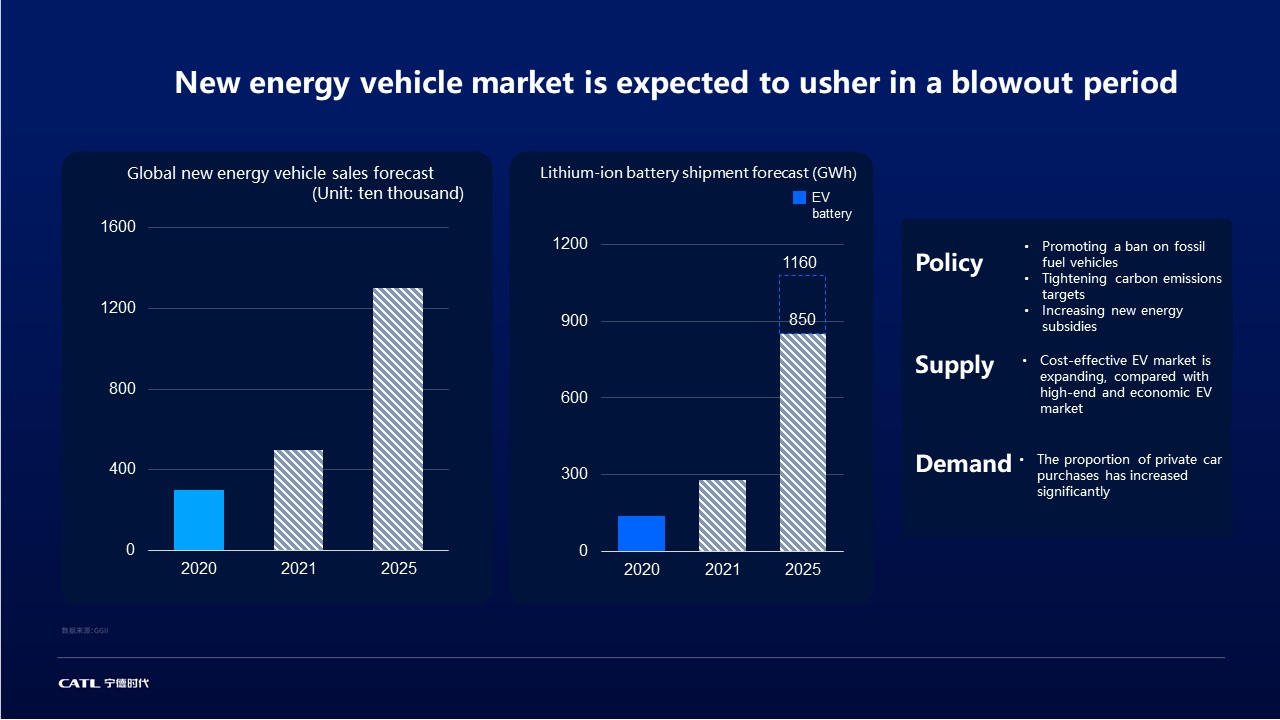

The two charts indicate that the NEV is greeting a market boom. According to GGLB, the consumption volume of the lithium-ion battery will reach 850 GWh (equivalent to 13 million vehicles) in 2025, and SNE research estimates that the consumption volume will reach 1160 GWh, implying a leap-frog transformation of the power battery market from the GWh-scale to the TWh-scale.

“Electrification + intelligentization” innovative application is widely used in an increasing number of scenarios, including electric vessels, smart battery swap solutions for heavy-duty trucks, and electric smart unmanned mines, etc. The combination of electrification and intelligence truly brings a lot of opportunities.

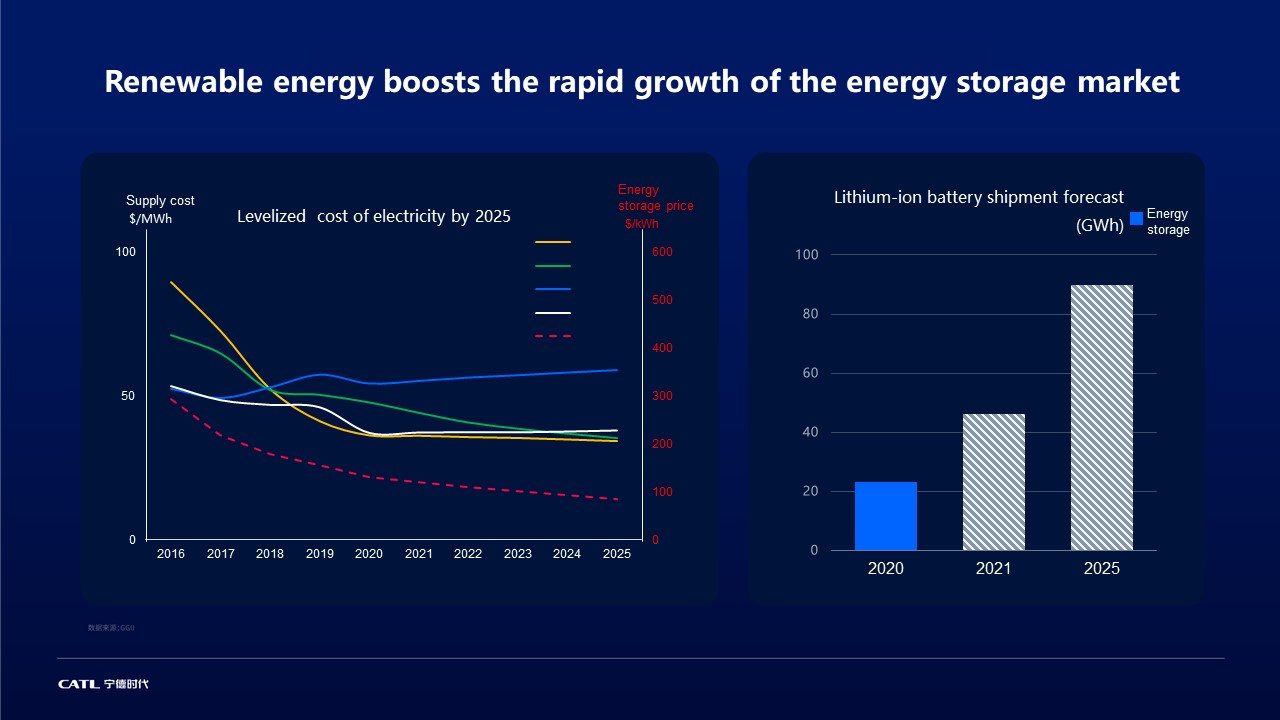

The cost of power generation by renewable energy keeps on decreasing, and the economic benefit of renewable energy will become more and more enhanced. The cost of generating solar and wind power continues to decline, closing to a level on par with that of fossil energy. China announced that by 2030, the total installed capacity of wind energy and solar energy will exceed 1.2 billion kW, namely, 1.2 TW, implying a massive energy storage development.

As the lithium-ion battery industry will enter the era of TWh by 2025, how can we benefit from this market?

During the international oil crisis in the 1960s, the world embarked on the study of hydrogen energy, but no solutions were found to store hydrogen in the materials and burned for driving. For this reason, the current hydrogen fuel cell mode was adopted, with a steel cylinder of 700 Mpa installed in vehicles. Lithium-ion battery makers like us started with the production of small battery cells like cells for mobile phones, and we never imagined that the small lithium-ion battery can even power a heavy vehicle. In this sense, we were lucky enough to discover that the lithium-ion battery can power large vehicles, even vessels.

As we are entering the era of TWh, we have to build up core competitiveness to maintain our leading position.

Innovation leads to core competitiveness

CATL's business focus is on three main directions: Firstly, we plan to leverage renewable energy and energy storage to replace stationary fossil fuel energy, thus contributing to the new energy industry; secondly, we leverage the EV battery to replace mobile fossil fuel energy to contribute to carbon neutrality; and finally, to promote the integration innovation of market applications leveraging electrification + intelligentization such as unmanned mines solution, electric heavy-duty trucks, electric vessels etc. In order to achieve sustainable development in these directions, we have established a four-dimensional innovation system in the material chemistry structure system, system structure, extreme manufacturing and business models as our core competitiveness.

Firstly, material chemistry structure system innovation is of great importance and we spend a lot of effort on it. Today, the mainstream material we use to produce EV batteries are LFP and NCM. Surely, these materials are fundamental, and they will predominate in the era of 1TWh. What about after the era of 1TWh? Something new might occur. We hope that we could avoid using rare metals and carve out a more cost-effective path to cope with the following 1.5TWh, 2TWh, and 3TWh. We will conduct an analysis from the atomic level to further comprehend the materials’ intrinsic properties and interface properties, in order to make fundamental innovations in the material system.

The second is system structure innovation, including CTP (Cell to Pack), CTC (Cell to Chassis) etc., mainly by optimizing the structure system and improving integration to achieve a reduction in system energy consumption and cost, and improve efficiency.

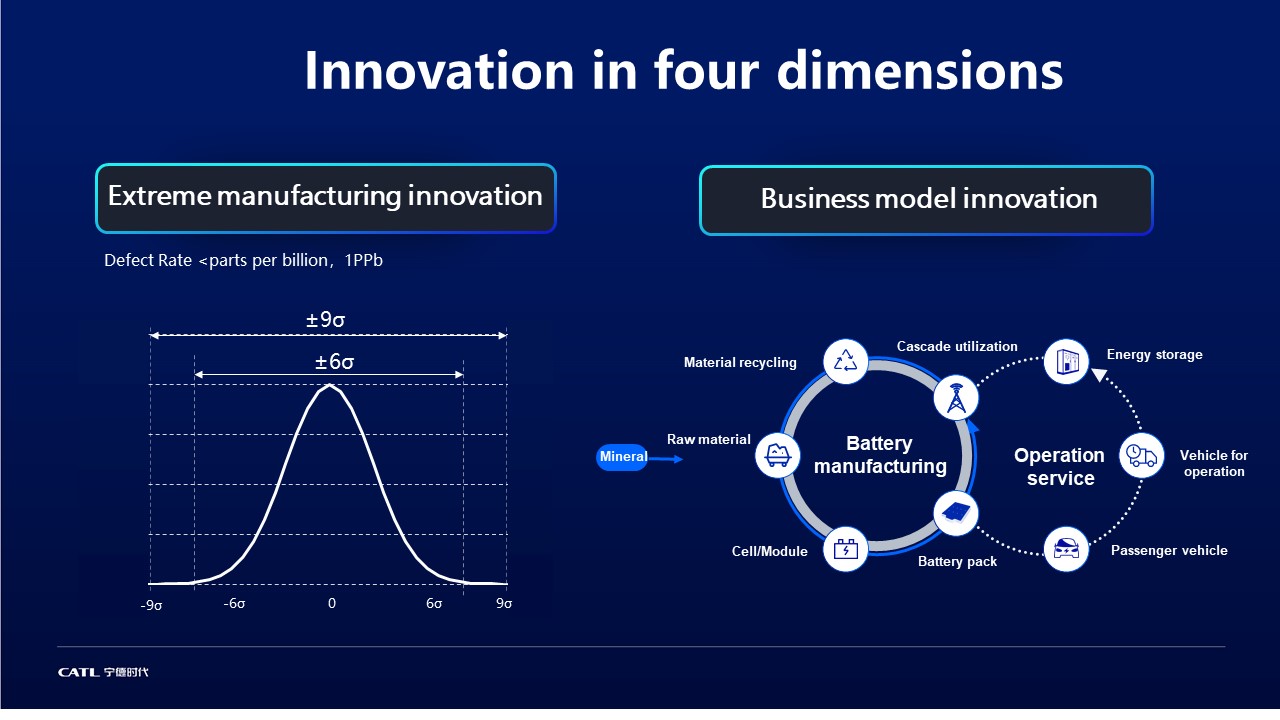

The third is extreme manufacturing innovation. The original six sigma standard for the manufacturing process is not enough to ensure the battery’s safety performance, so more innovations in manufacturing are required.

We need to achieve two objectives: firstly, the performance of the battery cell defect rate should be improved from the PPM (parts per million) level to PPB (parts per billion) level by three magnitude orders. Secondly, to ensure the reliability of the whole battery life cycle: How does the cycle life evolve from one cycle to 10,000 cycles after 20 years? How about the distribution of the orifices? We need to complete these fundamental studies to achieve the goal.

The fourth innovation is in the business model: In the future, we will have a lot of cooperative partners in the whole industrial chain including raw materials, battery production, operation service, and material recycling. It requires the formation of a complete value chain to ensure the sustainable development of the lithium-ion battery industry in the TWh era.

Industrial chain coordination to take up new challenges

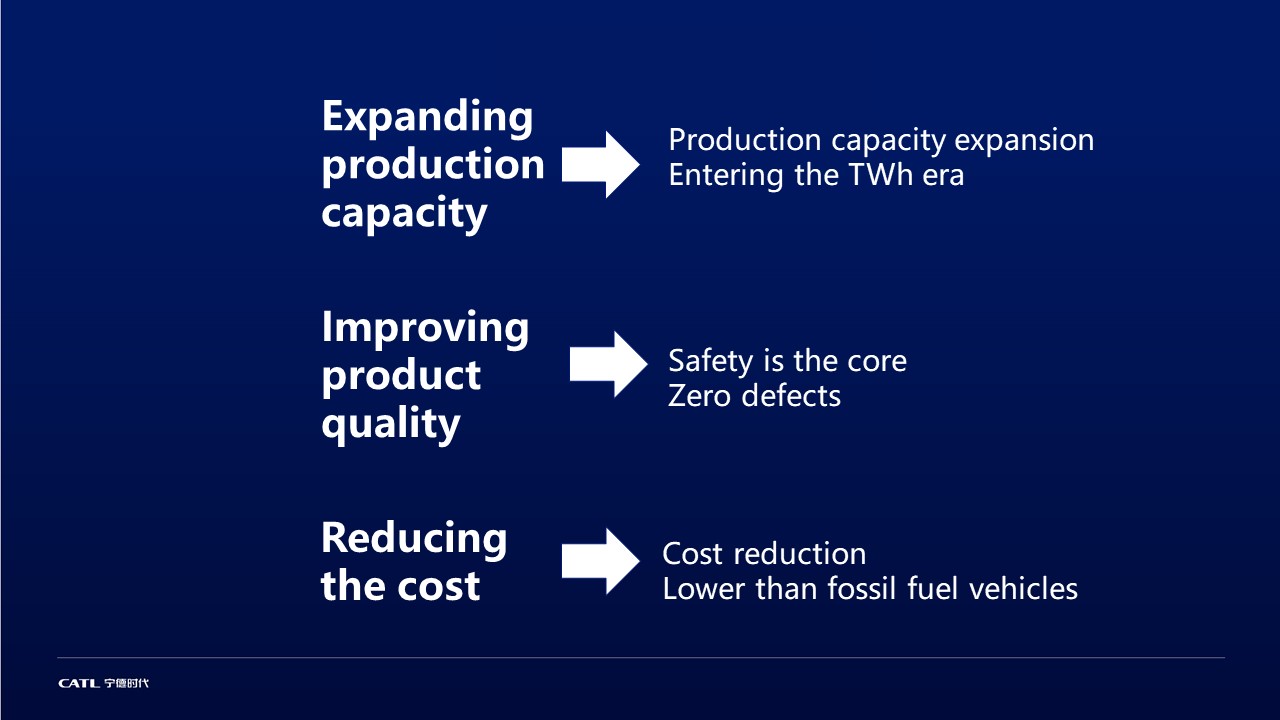

Currently, there is a huge gap between supply and demand. In 2025, demands for NCM and LFP materials, separators, electrolytes, and anode materials will be very different from the existing effective production capacity. Due to this reason, I advocate that we should make more efforts to carry out more effective production capacity to meet supply, with the increasingly larger and higher demand.

High-efficiency and high-quality delivery is a core competitiveness of our supply chain. Upstream and downstream players must work together to achieve the synergy to take up the challenges, to expand production capacity, improve quality and bring down the cost. Firstly, we should expand the production capacity to face the era of TWh-scale production. Secondly, we need to improve the quality, and keep in mind that battery safety is our lifeblood. We must insist on “Safety First” and seek to realize “Zero Defects.” Thirdly, we must reduce the cost, making the cost lower when compared to the fuel vehicle.

Lastly, I would like to stress that CATL's mission is to strive to deliver outstanding contributions to the green energy resolution for mankind. I genuinely hope that with our joint efforts, we can make this happen, Thank you!

By clicking on the button “I accept” or by further usage of this website you express consent with usage of cookies as well as you grant us the permission to collect and process personal data about your activity on this website. Such information are used to determine personalised content and display of the relevant advertisement on social networks and other websites. More information about personal data processing can be found on this link. Read More